Who Pays, Who Connects, Who Delivers

Large loads are forcing clearer rules on cost, interconnection, and accountability, without changing the mission.

Nothing here is new ideology. It’s execution.

Over the last two weeks, grid operators, regulators, and politicians have all circled the same issue from different angles: who pays for growth, how fast it connects, and how reliability is protected while it happens.

From Project Vanguard’s perspective, this is less about headlines and more about tightening the rules of the engagement.

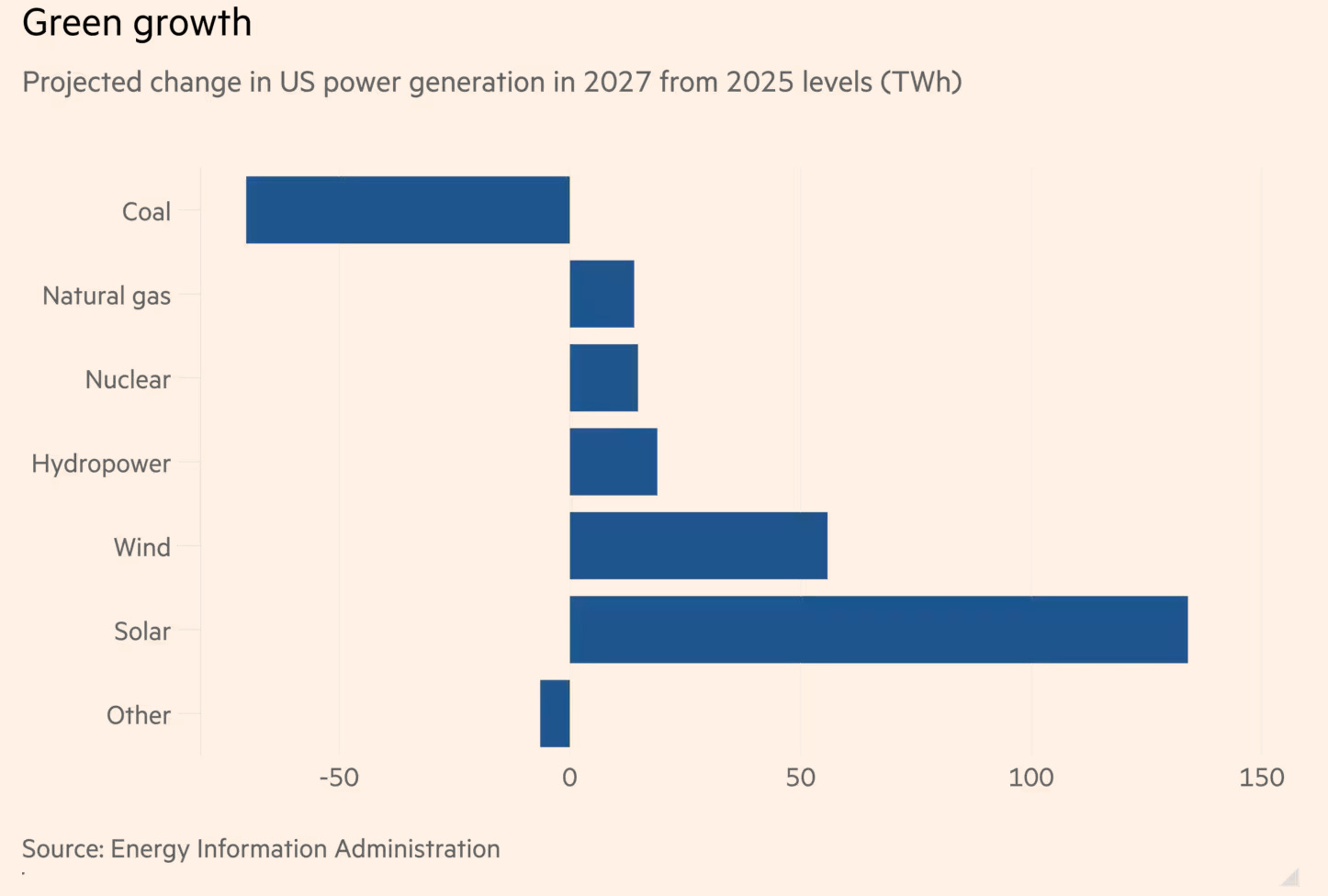

US green energy growth is proving hard to kill - Financial Times

The FT’s core point is not optimism, it’s inertia. Even after a sharp political shift in Washington, the underlying trajectory of the US power sector has not flipped. It’s not about picking winners and losers, it’s about battlefield conditions and maximizing force projection (regardless of the technology source).

“Despite a sharp adverse shift in federal policy — the growth is expected to come from renewables. The EIA predicts US solar generation will increase 46 per cent in the next two years. Wind power — hit by a welter of legally contentious government barriers — is still forecast to grow by 12 per cent.”

The article anchors that claim in demand growth first, not ideology.

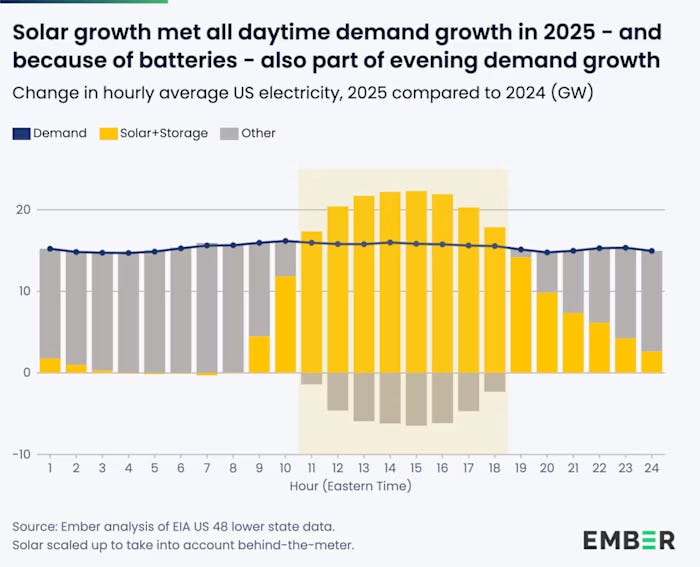

“Advances in battery technology and deployment are also helping to address the biggest weakness of solar and wind power: intermittency. The US had 45 gigawatts of utility-scale battery storage installed at the end of 2025 — up from 26GW a year before.

That might seem small when set against the US grid’s total generating capacity of 1,300GW. But the battery boom means that stored solar power is now meeting a significant proportion of US electricity demand growth even at night, as a new report from think-tank Ember explains.

And the trend is set to continue, with another 22GW of new battery capacity expected to come online this year, according to the EIA.”

Operator takeaway: This isn’t a story about politics winning or losing. It’s a story about what the grid keeps selecting under pressure. Solar keeps showing up because it can be built quickly. Batteries keep showing up because they solve a real operational problem. Gas remains a reliable part of an all of the above American Energy Dominance strategy.

Utilities under pressure: 6 power sector trends to watch in 2026 - Utility Drive

Utility Dive’s takeaway is straightforward: utilities are being squeezed from all sides, rising demand, cost pressure, and regulatory uncertainty, and are adjusting how they plan and operate. They are also coming into the crosshairs politically since rising bills have their names on them.

“Major policy changes in the One Big Beautiful Bill Act, which axed most subsidies for clean energy and electric vehicles, are forcing utilities, manufacturers, developers and others to pivot fast. The impacts of those changes will become more pronounced over the coming months.

Market forces will also have their say. Demand for power has never been greater. But some of the most aggressive predictions driving resource planning may not come to pass, leading some to fear the possibility of another tech bubble.

At the same time, each passing day brings more distributed energy resources onto the grid, increasing the opportunities — and expectations — for utilities to harness those resources into a more dynamic, flexible and resilient system.”

The six trends:

Large loads dominate planning

Renewables keep growing, even under policy headwinds

Flexibility becomes a near-term solution

Utility spending faces tighter scrutiny

Electricity prices keep climbing

Storage shifts from optional to standard

Operator Takeaway: This isn’t a reinvention year. It’s a filtering year. Big loads are being screened harder, flexibility is becoming a requirement, and anything that raises costs without improving reliability is getting questioned. Teams that plan for curtailment, storage, and cost discipline will move.

PJM and FERC closing the gap - Reuters | K&L Gates

PJM’s board outlined how it plans to handle AI-driven load growth without sacrificing reliability. The emphasis is on conditions, not denial.

“PJM Interconnection said it plans to require new large power users to either bring their own power generation or enter into a connect and manage framework subject to early curtailment.

Earlier in the day, the White House urged the largest U.S. electric grid to conduct an emergency power auction to protect against rolling blackouts as energy demand from data centers grows faster than the country can build new generation plants.

PJM’s measures include improving load forecasting and expanding the role for states, fast-tracking interconnections for state-sponsored generation projects, launching a backstop procurement process to address near-term reliability needs and reviewing PJM’s markets to better support investment.”

At the same time, FERC told PJM its existing tariff framework for co-located generation and load was not workable.

“FERC found PJM’s tariff to be unjust and unreasonable because it lacks clear rates, terms, and conditions of service for co-location arrangements.

PJM, which operates the nation’s largest electric grid across 13 states and the District of Columbia, has struggled to plan for and manage the significant increases in power demand from data centers. This order may prove to be a pivotal development for data centers: It potentially opens new pathways in PJM for integrating large loads with co-located generation. By directing PJM to clarify interconnection procedures and create new transmission services, FERC is enabling cost-effective project configurations that can accelerate development timelines, maintain grid reliability, and support innovative business models for both data centers and generation developers.

In regulatory parlance, a co-located load is an electrical configuration where an end-use (retail) customer load is physically connected to the facilities of an existing or planned generation facility”

Taken together, this is part of fast moving world that RTO/ISO have been thrust into in the last year.

Opeartor takeaway: This is not a slowdown signal. It’s a rules clarification phase. Co-located generation, conditional service, and staged firmness are becoming standard tools, not exceptions.

Cost allocation is moving upstream to the load - Financial Times

The push for emergency auctions and long-term contracts that force large loads to underwrite new capacity is about one thing: shifting risk.

“The administration along with governors of states including Pennsylvania, Ohio and Virginia have urged PJM — which serves more than 67mn people in the US north-east and Midwest — to hold a power auction in which big data centre operators bid for 15-year contracts to build new power plants.

Such contracts could support the construction of about $15bn worth of new power plants, with tech companies paying for them regardless of whether they use the resulting electricity, a White House official confirmed.”

This isn’t about punishing tech. It’s about preventing cost socialization from becoming politically untenable.

Operator takeaway: Expect more “load pays” structures. That favors disciplined builders and operators who can execute to contract terms over long timelines.

More Power That’s Faster and Fairer (Roundtable) - Energy Capital Podcast

This is a great Texas-first energy podcast, and this episode marks a shift in format as the show moves into a new chapter with new hosts and a roundtable-style discussion. I’ll always be a big fan of Doug Lewin and what he’s built. It’s great to see the platform growing, even as he moves onto a new chapter with Google.

The conversation stays grounded in Texas realities. Load is arriving faster than the grid can plan and build, and the hosts focus on what that means for reliability, transmission, and cost allocation in an energy-only market. Data centers are part of the story, but the real focus is speed and uncertainty.

It’s a strong listen if you want a practical, state-level view of where grid debates are heading next, without getting lost in national talking points.